Weekly Update: The AI Trade Is Over… For Now

Good evening, and welcome to this week’s edition of Stealth Trades!

For the last three years, investors have been focused on one thing – artificial intelligence.

Nvidia (NVDA) was the Wall Street darling and primary beneficiary of trillions in new AI spending.

Real estate investment trusts who owned data centers also did well. So did the companies who built the wiring, software and infrastructure that supports it.

But that is now what we call a “crowded trade.” Everyone is knee deep in AI stocks. And Wall Street is getting out.

The last 90 days has been a rotational period for the markets. All this means is that money managers are selling some groups of stocks and rotating into others.

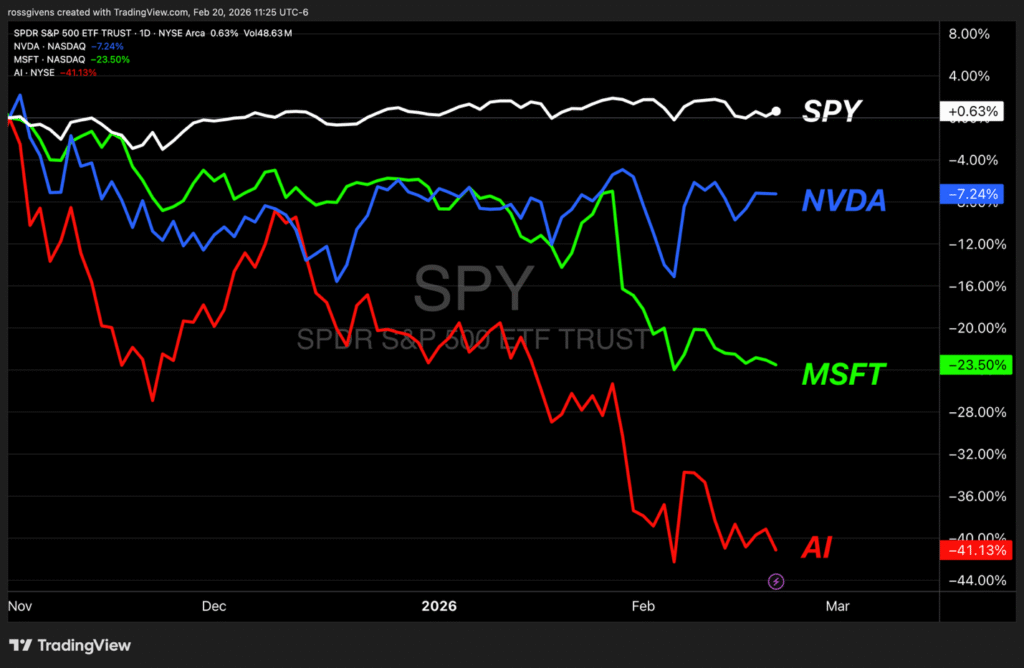

Below is the 3-month performance of the S&P 500 against Nvidia, Microsoft and C3.ai – three of the leading stocks of the AI market.

The picture is crystal clear.

The AI trade is over.

I expect to see these former leaders go even lower in 2026. That, afterall, is the historic precedent for new technologies.

Hype and optimism drive leading stocks to unreasonable valuations. They trade for prices that reflect perfect execution and exponential growth.

Put simply, the stocks go up too much too fast.

Then they come back to reality. Profit taking and institutional rotation drive prices lower, and they fall until prices are reached that reflect a discount to true value.

Dario Amodei is the CEO of Anthropic – the company behind the popular Claude AI model. In a recent interview, he laid out the single biggest financial risk in AI right now.

It’s not whether the technology works. He’s pretty confident it will. The risk he sees is whether the money comes back fast enough to justify what’s being spent.

He laid it out like this…

Anthropic has been growing at roughly 10x per year. They went from about $1 billion in early 2025 to around $9 billion by end of 2025 to $14 billion annualized as of February 2026.

That growth is insane.

But he can’t just assume it keeps going at that pace forever.

If revenue keeps growing 10x a year it would hit $100 billion by the end of 2026 and $1 trillion by the end of 2027.

If he bought a trillion dollars’ worth of computers based on that assumption and revenue came in at even $800 billion instead, there is no hedge on earth that saves him from bankruptcy.

Being off by just 20% when you’ve committed that much capital is fatal.

If the growth rate slows to 5x instead of 10x, or the timeline shifts by just one year – same result.

You’re basically done.

Even if AI becomes genius level in the lab, turning that into actual revenue takes time.

Amodei uses the example of disease….

AI might discover cures for everything, but you still have to manufacture the drug, run clinical trials, get regulatory approval and distribute it globally.

COVID vaccines took a year and a half to reach everyone even with the entire world in a panic.

Polio has had a vaccine for 50 years and still hasn’t been fully eradicated.

The technology being ready and the revenue actually showing up are two very different timelines.

So, what does he do?

He deliberately under buys. He commits to hundreds of billions in infrastructure, not trillions.

He accepts the risk that if demand explodes, he won’t have enough capacity.

Because he’d rather leave money on the table than bet the entire company on a growth curve that might be off by a year.

But not every tech company is showing the same restraint…

Some of the other AI companies are just throwing money around without doing the math. Committing $100 billion here, $100 billion there, without actually modeling what happens if revenue comes in below expectations.

He calls it YOLOing – a term us traders are familiar with.

For context, Big Tech is expected to spend around $625 billion on AI infrastructure in 2026 alone.

AI services are only generating about $25 billion in actual revenue against all of that.

That’s roughly a 4% return on what’s being invested.

The gap between what’s being spent and what’s being earned right now is massive. And therein lies the problem.

This is the same dynamic that wiped out dotcom companies in the early 2000s.

They built the infrastructure for demand that eventually came, but it came too late to save many of the companies that built it.

Today’s stock prices – the valuations of these hot young AI companies – are out of touch with reality. They reflect years of future growth that has not yet happened.

OpenAI, for example, did $20 billion in revenue last year. Yet it has $1.4 TRILLION in spending commitments.

The math isn’t mathing.

He thinks his company is too big to fail. He’s wrong. It will.

Others will end up being the best investments of all time. But only when the price makes sense.

In all likelihood, they will see a correction first.

And when that happens, I’ll be looking to buy; to make long term investments in what will be massively successful companies over the next 10-20 years.

In the meantime, my advice is to avoid too much exposure to AI in your investment accounts.

Most index funds which are market cap weighted. Big companies like Nvidia and Microsoft get a disproportionally large chunk of your investment dollars.

They can suffer big losses if the top 5 or 10 stocks fall off.

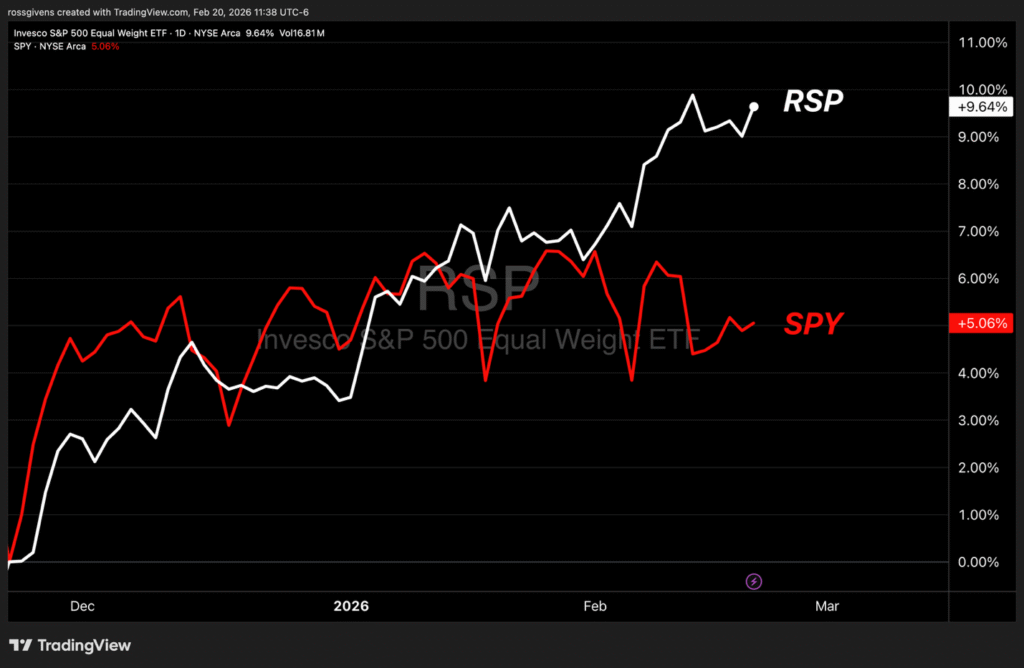

A simple way to avoid this is with an equally weighted fund like RSP. RSP is the Invesco S&P 500 Equal Weight ETF. All 500 stocks in the index are given the same weight.

Over the last 90 days, RSP has delivered nearly doubled the returns of SPY.

It continues to make new highs, even though Microsoft, Amazon and Apple are in free fall.

In Monday morning’s live session, we will do a deeper dive into the leading areas of the market to identify where money is flowing and hopefully identify some new opportunities.

I’ll see you then.

Best wishes for your trading,

Ross Givens