Weekly Update: Insider Betting $12.5 Million On This Stock

Good evening, and welcome to this week’s edition of Stealth Trades!

One of the most reliable signals you will find is insider buying in a stock.

The logic is simple…

Insiders know everything about their company. They know the sales and earnings before they’re reported publicly. They know about mergers and buyouts long before the whispers start. They know the results of their drug trials weeks before the press conference.

So, if they are buying their stock – while privy to such private, market moving information – it may be a sign that good news is coming.

I have run a paid service since 2017 called the Insider Effect. It has significantly outperformed the stock market for nearly a decade. And all we do is look for signs of clear, opportunistic insider buying activity.

Are they all winners? No.

But it is rare to see a big loser. If a company were about to report terrible sales, a failed drug trial, or some other disastrous corporate event, do you really think the top executives would be buying their stock? At current market prices?

Absolutely not.

Now, I almost never share my top insider picks for free. Afterall, we have winners who spent thousands to get that research.

But this morning I shared one on YouTube. And I wanted to be sure you saw it as well.

Members got this information weeks ago. And to my loyal Insider Effect subscribers, don’t worry – this will not be routine.

But I want everyone to see the information that is available to them.

Below is the official buy alert sent to members on June 4. The stock, AUPH, still trades within a few percent of where it was at that time.

Aurinia Pharmaceuticals Inc. (AUPH)

Aurinia Pharmaceuticals Inc. (AUPH) is a commercial-stage biotech focused on autoimmune kidney disease and related autoimmune conditions.

Its main drug is LUPKYNIS, the first FDA-approved oral therapy for adults with active lupus nephritis – a serious complication of lupus where the immune system attacks the kidneys.

As is common in biotech, most insider activity tends to be selling (due to heavy stock-based compensation as a result of company cashflow constraints).

But Aurinia has caught the attention of one insider – Kevin Tang – who has been moving in the opposite direction.

Tang is no ordinary biotech insider.

He is the founder of Tang Capital Management, a life-sciences investment firm with a long history of investing in, controlling, acquiring, and restructuring biotech companies. Over the years, Tang has helped build or back companies including Ardea Biosciences, La Jolla Pharmaceutical, Odonate Therapeutics, Heron Therapeutics, and Concentra Biosciences.

His playbook is to look for biotech assets the market is undervaluing – then build influence, push for leaner operations, and drive some kind of strategic transaction.

That is exactly what appears to be happening at Aurinia.

Over the past few years, Tang has been accumulating AUPH shares. Then in early 2026, after another large open-market purchase in March, he amassed enough influence to take over as CEO and reshape the company around his own team.

Tang replaced the prior CEO, helped overhaul the board, reduced the number of directors from nine to six, and installed a much leaner compensation structure. He also elected to receive no salary, bonus, equity awards, or other compensation from Aurinia.

That is a very different setup from the old regime.

Then, almost immediately, he used Aurinia to acquire Kezar Life Sciences – a biotech he had apparently been eyeing for some time through another Tang-linked vehicle.

So this is not just an insider buying stock.

This is an activist biotech investor taking control of the company, cutting costs, reshaping leadership, and using Aurinia as a platform to consolidate autoimmune assets.

And he is still buying.

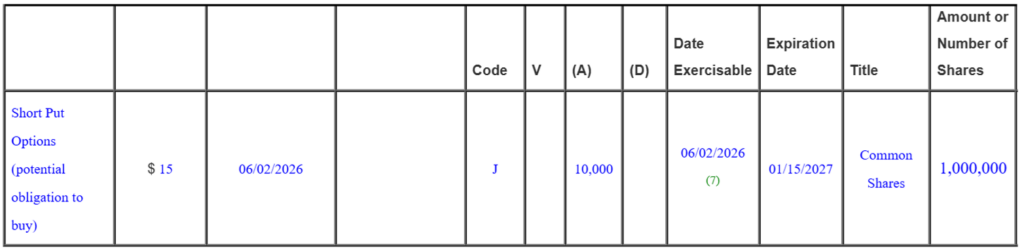

Earlier this week, on June 2, Tang bought another roughly $12.5 million worth of AUPH shares on the open market – bumping his stake in the company up to 10%.

At the same time, he also sold 10,000 put options, creating a potential obligation to acquire up to 1,000,000 additional common shares at $15 per share if exercised by January 15, 2027.

That is a clear statement of conviction.

Tang is not just adding shares – he is effectively underwriting more potential exposure around the same price level.

So what could be underlying his conviction in AUPH?

The first piece is LUPKYNIS.

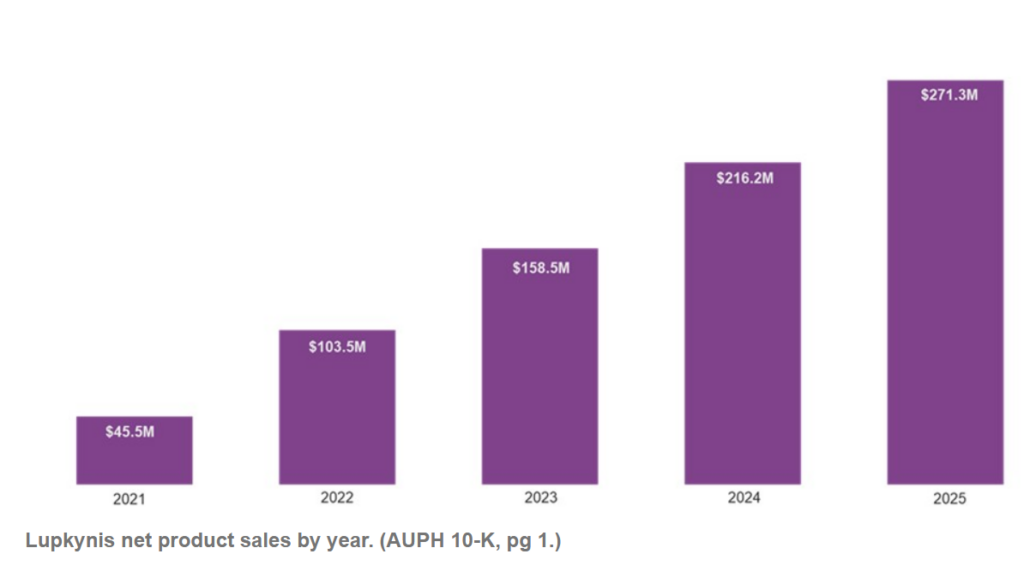

In 2025, LUPKYNIS generated $271.3 million of net product sales, up 25.5% from the prior year. In Q1 2026, it generated $73.6 million of net product sales, helping Aurinia produce $77.7 million of total revenue, $34.4 million of net income, and $32.6 million of operating cash flow. Management is guiding for $305 million to $315 million of LUPKYNIS sales in 2026.

So the base business is still growing.

That alone gives Aurinia a much stronger foundation than a typical clinical-stage biotech. The company ended Q1 with nearly $379 million of cash, cash equivalents, restricted cash, and investments. It also repurchased 12.2 million shares in 2025 and another 2.5 million shares in Q1 2026.

In other words, Aurinia already has a cash-generating commercial drug, a large cash balance, and a management team now focused hard on capital allocation.

The second piece is market potential.

Aurinia says more than 200,000 people in the U.S. have systemic lupus erythematosus, and roughly 20% to 60% of them develop lupus nephritis. That implies a large U.S. lupus nephritis patient pool before even counting international markets handled through partner Otsuka.

And LUPKYNIS still appears to have runway.

The drug has not plateaued five years into launch. It continues to grow. And updated lupus nephritis treatment guidelines increasingly support early aggressive therapy, including approaches that can include a calcineurin inhibitor – exactly where LUPKYNIS fits.

The third piece is Aritinercept.

Aritinercept is Aurinia’s next autoimmune asset. It targets both BAFF and APRIL, two pathways involved in B-cell-driven autoimmune disease. The company believes that dual blockade could give it broader immune control than drugs targeting only one pathway.

Aurinia has already completed a Phase 1 single ascending dose study, where the drug was well tolerated and showed durable immunoglobulin reductions that support the possibility of once-monthly dosing.

More importantly, Aurinia has now said Aritinercept is in clinical development for three potential autoimmune indications.

That gives the company multiple chances to expand beyond lupus nephritis.

The fourth piece is Kezar.

In March, Aurinia agreed to acquire Kezar for $6.955 per share in cash plus a contingent value right. The key asset is Zetomipzomib, a first-in-class immunoproteasome inhibitor being developed for autoimmune hepatitis, lupus nephritis, and systemic lupus erythematosus.

Kezar had already reported encouraging Phase 2 autoimmune hepatitis data and had a constructive FDA Type C interaction.

This acquisition gives Aurinia another shot on goal in autoimmune disease – and it fits Tang’s broader pattern. He appears to be using Aurinia’s cash flow and balance sheet to build a larger autoimmune company, not just milk one commercial drug.

That creates several potential catalysts.

LUPKYNIS can continue showing commercial growth. Aritinercept indications can be disclosed or advanced. Kezar can close and be integrated. Zetomipzomib can move toward a clearer FDA path. And Tang could pursue additional strategic moves if he sees more undervalued assets in the autoimmune space.

There is also the possibility of a larger strategic transaction down the road.

Tang has a long history of dealmaking. And while that is no guarantee – it does mean investors should view Aurinia differently now. The company is no longer run like a sleepy specialty pharma waiting for LUPKYNIS to mature. It is now under an operator who has repeatedly used biotech companies as vehicles for transactions, restructurings, and exits.

Valuation also looks reasonable. AUPH trades at a modest multiple of trailing sales compared with many commercial rare-disease and specialty biotech names.

Price action is also looking constructive.

Since April, AUPH appears to have formed a bull flag / wedge pattern. The stock consolidated tightly after a prior move higher, and yesterday it looked to have broken out of that range – simultaneously reclaiming both its 21-day and 50-day moving averages (blue and red lines on chart).

Aurinia is now under a capital-allocation-heavy, strategically opportunistic leadership team. And Tang just keeps increasing his exposure.

Given Tang’s open-market purchases, his put-sale commitment, his history of biotech dealmaking, the continued LUPKYNIS growth, the Aritinercept and Kezar pipeline optionality, the modest valuation, and the constructive breakout setup, Aurinia Pharmaceuticals (AUPH) makes a compelling investment.

Best wishes for your trading,