Weekly Update: We Just Got BIG News for The Stock Market

Good evening, and welcome to this week’s edition of Stealth Trades!

Inflation is getting better. The job market is getting worse.

And this combination of declining inflation and a weakening job market means we are almost guaranteed another interest rate cut in January.

Thursday morning, the US Bureau of Labor Statistics released the latest CPI number.

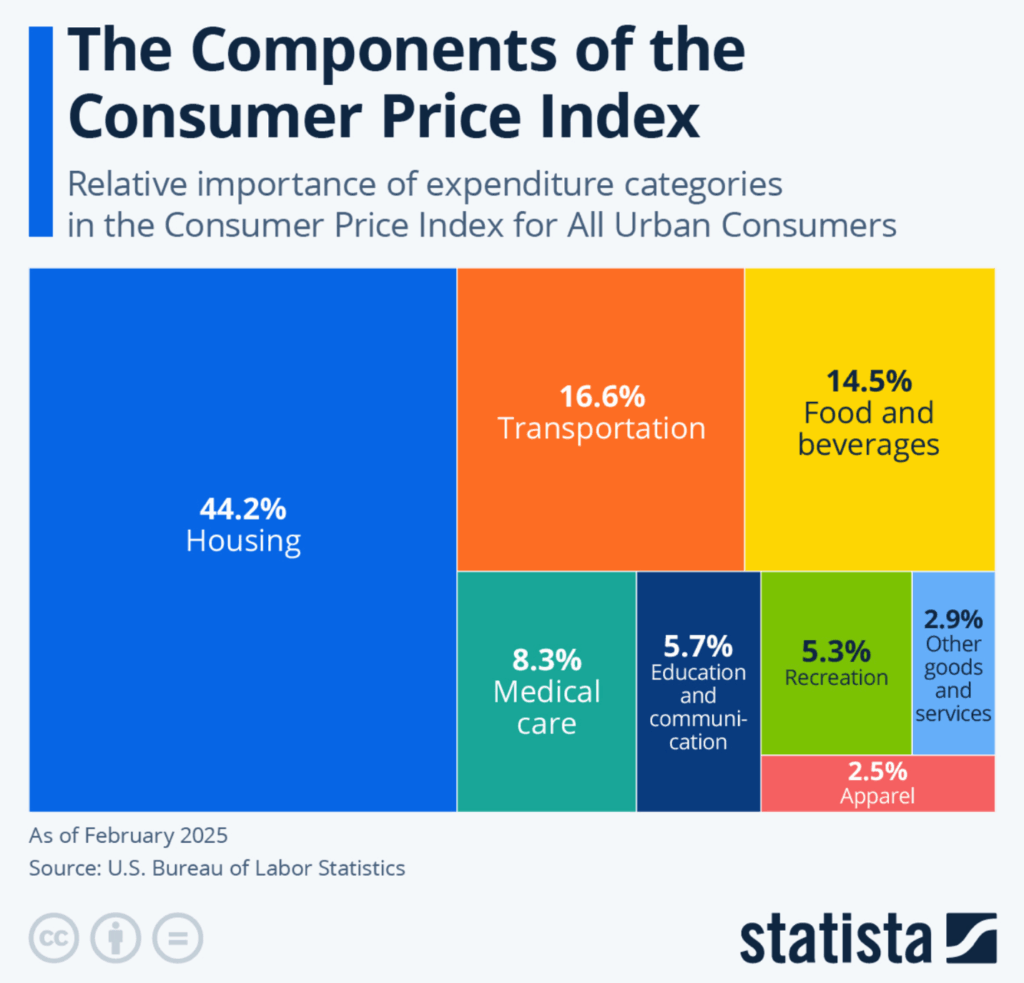

CPI stands for Consumer Price Index. It measures the change in prices paid by consumers for a basket of consumer goods and services.

It tracks the prices of housing, clothes, food, utilities and medical care – all the basic necessities.

And once a month, the US Bureau of Labor Statistics compiles this data and publishes the number. Inflation is how much this figure went up compared to the same month last year.

And shockingly, inflation came down in November. Prices were higher, but not by as much as they had been in previous months.

Core CPI, which is everything except food and energy prices which can be volatile, was up 2.7% year-over-year.

And while this is still above the Fed’s long-term 2% target, it is better than expected.

The August number was 3.1% – a new 6-month high.

September came in around the same at 3%.

There was no report in October due to the government shutdown, but most economists were forecasting around the same 3%.

So, 2.7% was a surprise… and a good one. But the ramifications are far bigger than saving 10 cents on beef at Piggly Wiggly.

It means the odds of a January rate cut just went way up.

Because lower-than-expected inflation isn’t the only piece of news we got this week.

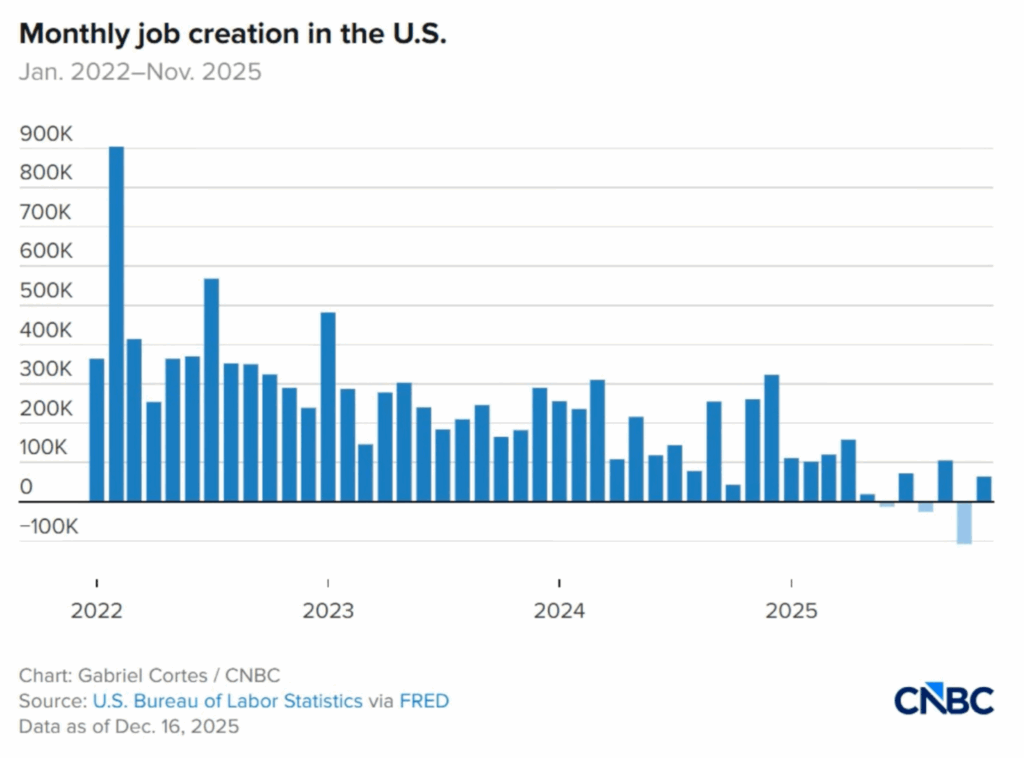

On Tuesday, a new jobs report was released.

And it showed that the US labor market continues to weaken.

They released data for October and November at the same time.

The US lost 105k jobs in October and gained 64k in November – a net DECLINE of 41k jobs.

Look at the trend over the last four years.

These are the jobs added on a monthly basis since 2022.

You don’t need to be an economist to see that the job market is in trouble. The numbers are steadily declining.

But it’s the last 6 months where things have really taken a turn for the worse.

In 3 of the last 6 months, the US economy has lost jobs. We haven’t lost people.

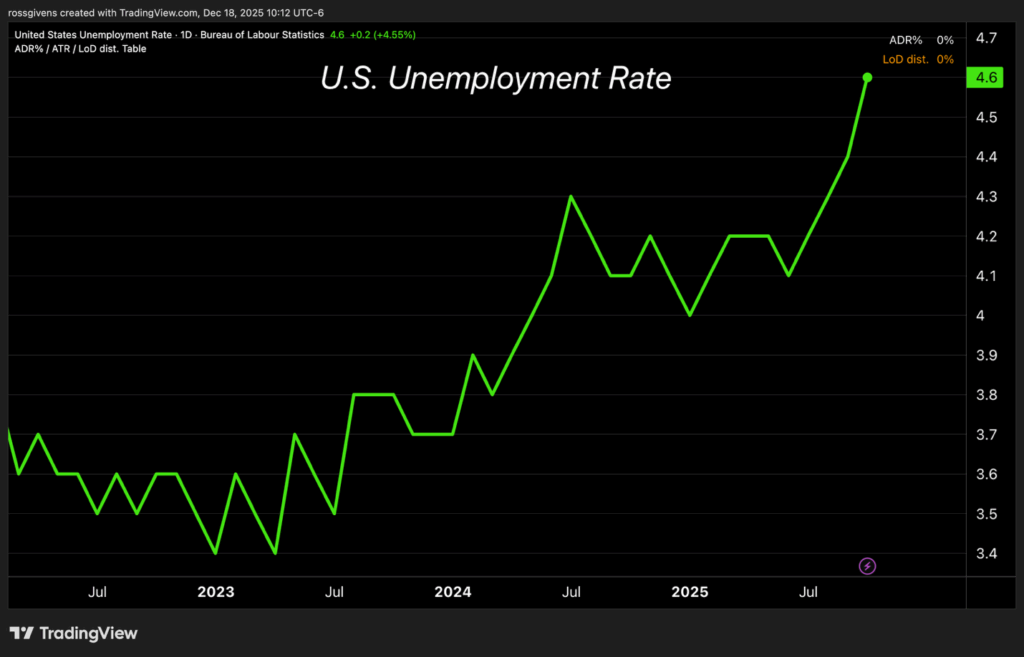

So, the unemployment rate is rising. It is at 4.6% and climbing.

Another thing to keep in mind is that these numbers are not accurate. They will most likely be revised downward and most perhaps heavily.

Back in September, we learned that the 2024 jobs numbers were overstated by 911k.

Nearly a million jobs that we thought were created vanished overnight.

Even Jerome Powell, the Chairman of the Federal Reserve, recently said that most likely these job figures are being drastically overstated.

Powell said that he suspects that the job numbers are overstated by as much as 60,000 jobs per month.

So the “official” data is bad. And the “real” data is probably even worse.

The weak labor market is why the Federal Reserve has been cutting interest rates – to stimulate the economy and create more jobs.

In my opinion, the only thing holding the Fed back from cutting by half or even three-quarter percent has been stubborn inflation.

Cutting rates into above-average inflation creates worse inflation.

And that has been the rock and a hard place the Fed has been stuck in all year.

On the one hand, inflation is high which means they should not cut rates.

On the other hand, the labor market is deteriorating. Unemployment is high and getting worse. They need to lower interest rates in order to stimulate the economy. As rates fall, consumers spend more, producers invest, and more jobs are created as a result.

So, this week’s data is giving them an out. The data is saying “it’s okay Jerome… you can cut… inflation isn’t that bad…”

Jerome Powell has said repeatedly that unemployment is the single most important data point for the labor market.

And that picture could not be any clearer.

Another metric the Fed looks at, when deciding on interest rates, is hourly wage growth.

And it’s not looking much better…

Hourly earnings rose 3.5% year over year.

You might think, “Well inflation is 2.7% but wages are up 3.5%, so the American worker is winning, right?”

Wrong.

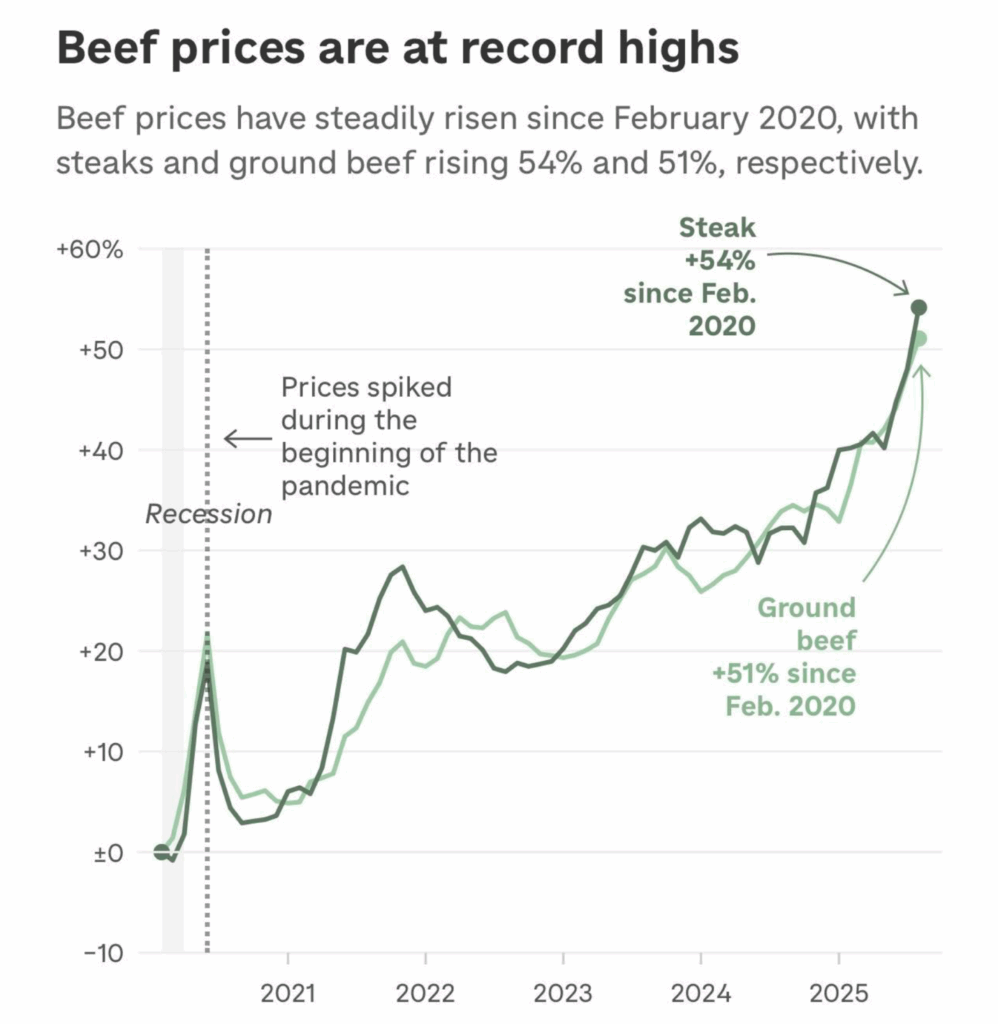

The real inflation is closer to 6%.

You see, the CPI basket – the goods and services tracked to determine inflation – has not seen a major revision since the 90s.

It doesn’t reflect consumer reality.

For example, what was your cell phone bill in 1995? Zero. Today it’s probably a couple hundred bucks. Things like childcare and medical costs eat up a much larger portion of incomes today than they did 30 years ago.

Beef and steak prices, which are a staple in my house, are up more than 50%.

So, if real inflation is closer to 6%, that means wages are not keeping pace with inflation. So not only are more people losing their jobs, but the ones that have them are seeing pay cuts in terms of actual purchasing power.

This week’s data is going to unshackle the Federal Reserve. Not only are we likely to see another 25bps rate cut in January, there is a chance we could see an even bigger 50bps cut as an emergency measure to rescue the labor market.

And while all of us benefit from lower interest rates in the short term, they are going to make inflation worse over the long term.

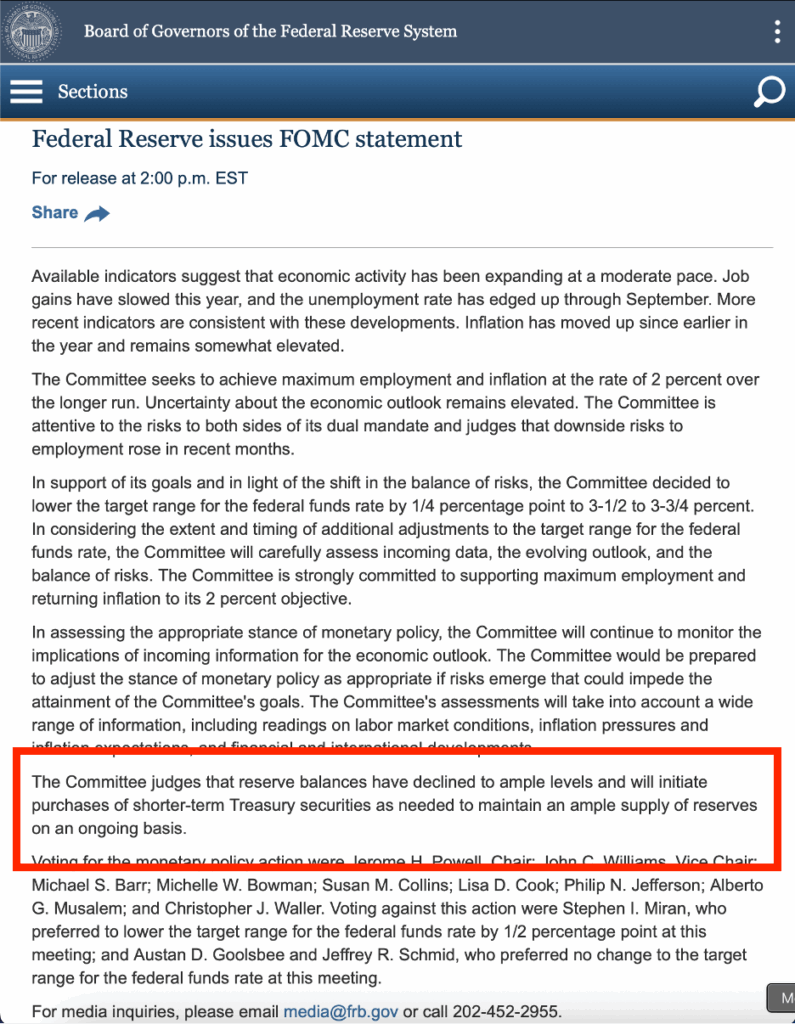

Especially with the Federal Reserve’s announcement that they would be turning the money printers on again.

Powell didn’t mention it. The Fed tried to downplay it. But here it is, at the bottom of the official press release.

The Fed is ending its policy of quantitative tightening. They are done shrinking the balance sheet.

And will now “initiate purchases of shorter-term Treasury securities as needed to maintain an ample supply of reserves.”

So, they’re going to start buying bonds. Powell says $40-$60 billion worth a month. Where do they get the money to buy those bonds?

They print it. It is created out of thin air. Billions of dollars of new money flooding the system.

And this produces, as it always has, only one possible outcome…

More inflation.

More dollars chasing the same number of goods and services makes prices go up. That’s it. It’s not any more complicated than that.

And that’s exactly what the Fed has done for the last hundred years.

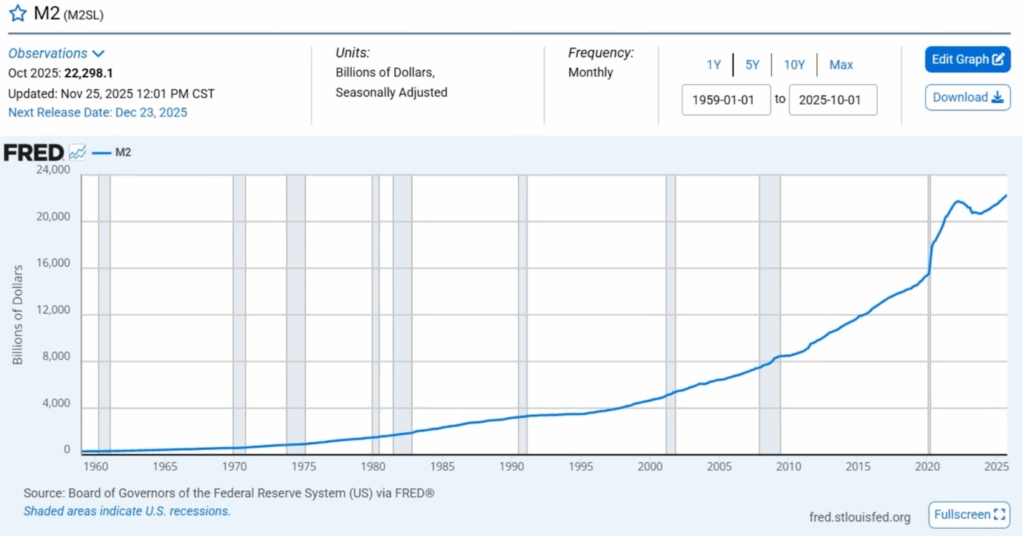

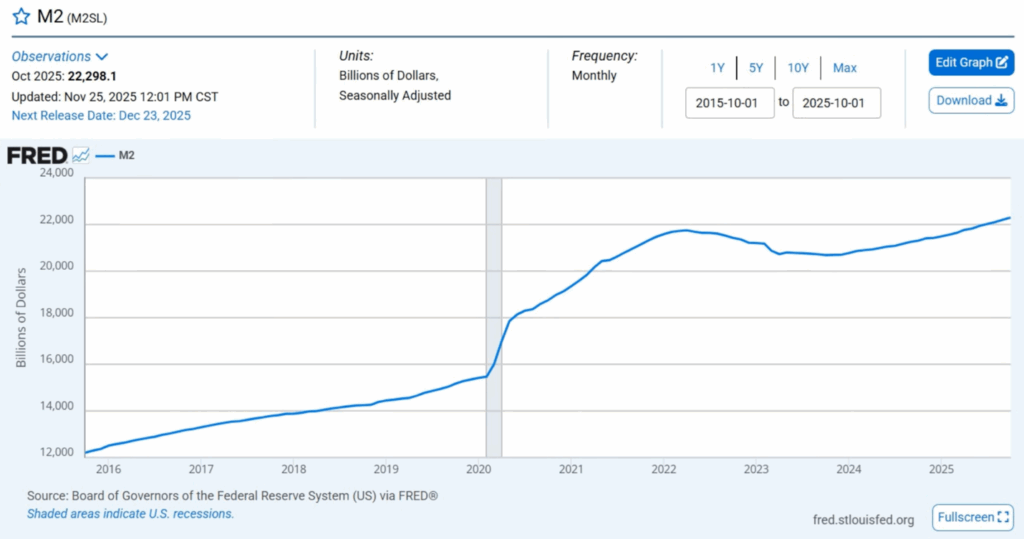

This is the M2 money supply – how much money is in the US economic system. $23 trillion and climbing.

Here’s a closer look at the last ten years…

You can see the huge jump in 2020 when the government printed trillions of dollars for stimulus and bailouts. They kept spending into early 2022 until the Fed pivoted and began shrinking its balance sheet.

Remember the 2022 bear market? This, coupled with big rate hikes to fight inflation, are what caused it.

Anyway, the money supply has been growing at an annualized rate of approximately 5%.

And that’s with healthy +3% GDP growth… in a period of rising interest rates with the Fed shrinking its balance sheet.

Now the money printers are turned back on.

Interest rates are being cut. So, there’s going to be even more money loaned into existence.

We also have a federal government with $2 trillion dollars a year in deficit spending. That’s 2 trillion dollars more than it brought in that has to be printed just to make ends meet.

Interest payments on our debt now exceed the defense budget.

Think about that for a second…

The US government pays more in interest… on money they already spent… than it spends on the military.

And heads up… it’s not going to get better. The spending, the deficit, our national debt… it’s only going to get worse.

So, what does all this mean going forward? Here’s my outlook…

Money printing, which the Fed is again doing, raises stock prices.

The same inflationary forces that drive up housing and food prices also push stock prices higher.

Lower interest rates are also good for stocks.

It lowers margin rates, brings in new money from money markets and fixed income, and allows stock valuations to rise and remain competitive with dwindling bond yields.

And with this month’s inflation report coming in lower than expected and a labor market on life support, the Fed will have no choice but to cut again in January – another quarter or even half percentage point.

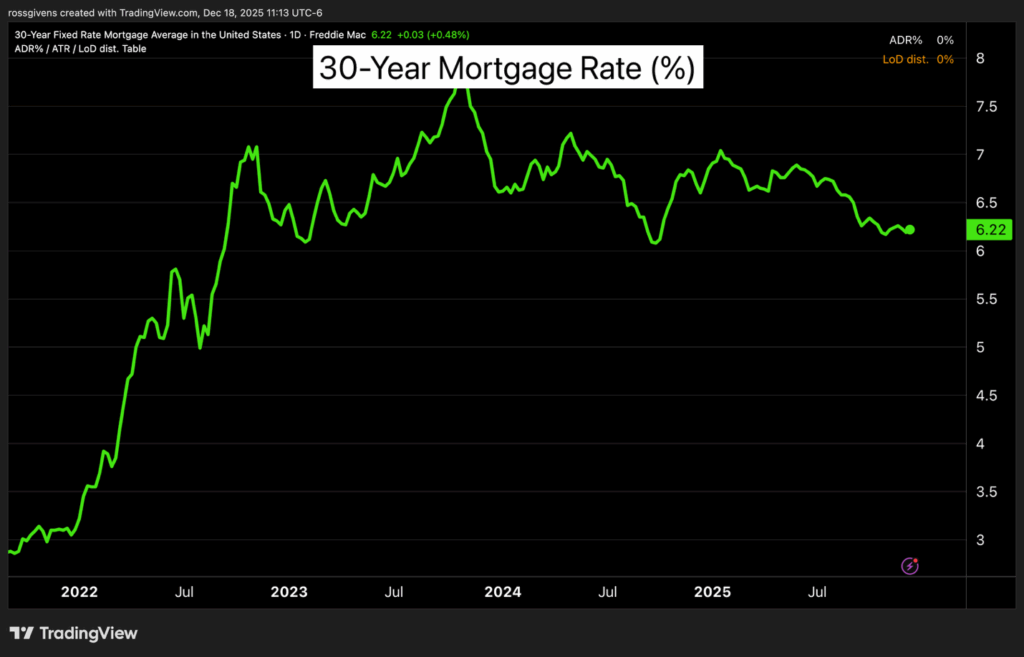

If you’ve been waiting to buy a house or refinance your 7% mortgage, 2026 will likely be your best opportunity.

Mortgage rates will likely fall into the high 5s in the first quarter and possibly to as low as 4.5% by the end of the year…

It just depends on how aggressive Trump’s new Fed Chair pick decides to be.

My guess is that he comes out swinging.

But when the inevitable inflation shows up, they’ll have no choice but to raise interest rates again. So don’t expect another 2021 scenario with 2.7% mortgages.

The writing on the wall is clear. This is one of the best times to own assets and a hugely bullish backdrop for the stock market.

Best wishes for your trading,